Part I — The Macroeconomic Stabilisation Paradox

Oyewole O. Sarumi PhD and Olusola O. Aliu PhD

Introduction

On 29 May 2026, President Bola Ahmed Tinubu delivered his third-anniversary address to the Nigerian nation. The speech was, by any standard of political craftsmanship, a disciplined and rhetorically sophisticated performance. It laid out, in measured cadence, a narrative of sacrifice rewarded, of pain endured, and stability won. Markets stabilised. Revenues reclaimed. Infrastructure mobilised. A nation, the President assured us, that had stepped back from the precipice now stood at the dawn of recovery.

This analysis, Part I of a two-part forensic examination, does not dispute the existence of reform. Where credit is due, it is given. What this paper does, however, is apply the rigorous tools of political economy, institutional analysis, and comparative developmental experience to interrogate the gap between the stabilisation metrics the speech celebrates and the lived realities that over 140 million Nigerians continue to navigate daily. We write not as partisans of opposition, but as scholars and practitioners who have studied, advised, and witnessed economic reform processes across Sub-Saharan Africa, Southeast Asia, South Asia, and Latin America, regions that have, in their own seasons, walked the same painful corridor between macro-stabilisation and citizen-level recovery.

Part II of this series, to follow, will address the more constructive and urgent question: how does Nigeria now build the bridge from macro-stabilisation to inclusive, grassroots recovery? That is the policy challenge that will define this administration’s historical legacy.

The forensic framework applied here draws on current data from Nigeria’s National Bureau of Statistics (NBS), the World Bank, the International Monetary Fund (IMF), the African Development Bank (AfDB), the Central Bank of Nigeria (CBN), Afrobarometer, the Food and Agriculture Organization (FAO), the Famine Early Warning Systems Network (FEWS NET), and a corpus of peer-reviewed and institutional research. We analyse the speech across nine domains: the macroeconomic architecture, the currency and forex regime, inflation and household costs, the power sector, agriculture and food security, infrastructure, youth and the brain drain crisis, security, and the political economy of the reform narrative itself.

I. THE POLITICAL ARCHITECTURE OF THE SPEECH: STABILISATION BEFORE PROSPERITY

President Tinubu’s address rests on a foundational premise that students of political economy will recognise from austerity cycles in Greece (2010–2015), Indonesia’s post-Asian Financial Crisis adjustment (1998–2002), and Ghana’s IMF-supported stabilisation programme (2022–2024): that short-term pain, if correctly administered, produces long-term macroeconomic stability, which in turn becomes the platform for growth and prosperity. This is classic ‘shock therapy’ logic, though the Tinubu administration prefers the softer framing of ‘reform before recovery.’

The speech is architecturally designed to accomplish three things simultaneously: to justify the reforms already implemented, to claim credit for macroeconomic indicators that are measurably improving at the aggregate level, and to purchase additional political patience from a citizenry that has endured three years of compressing real incomes. It is, in the language of statecraft, a legitimacy-restoration exercise, and a competently constructed one at that.

The critical forensic question, however, is not whether the speech is well-crafted. It is whether the stabilisation narrative accurately represents the full economic reality that Nigerians inhabit in May 2026, and whether the administration’s policy sequencing has been optimally designed and implemented to translate macro-level gains into household-level relief.

The answer, as this analysis will demonstrate, is decidedly mixed, and in several domains, deeply troubling.

II. THE SUBSIDY REMOVAL AND FOREX UNIFICATION: CORRECT DIAGNOSIS, POORLY SEQUENCED POST-SURGICAL CARE

Let us begin where the administration’s reform narrative is on its strongest ground. The petrol subsidy regime, as the President rightly states, had become fiscally catastrophic. By 2022, Nigeria was spending in excess of ₦4 trillion annually on subsidy payments, resources that could not be directed to capital investment, healthcare, or education. The NNPC’s own financial reporting had made clear that the subsidy had become a mechanism of elite rent extraction, with systemic corruption distorting volumes, prices, and accounting throughout the petroleum distribution chain.

Similarly, the multiple exchange rate windows, a legacy architecture that permitted connected individuals to access artificially cheap foreign currency for resale at market rates, represented one of the most regressive wealth-transfer mechanisms in contemporary African political economy. The IMF had explicitly identified exchange rate unification as ‘a critical step toward improving monetary policy transmission and restoring macroeconomic stability’ (IMF, 2023). The World Bank concurred that market-determined exchange rates would eliminate distortions while encouraging productive investment.

On both counts, subsidy removal and FX unification, the diagnosis was correct. The question that forensic analysis demands is not whether these reforms were necessary, but whether their sequencing, timing, and social cushioning were adequate. We respond that the social cushioning was not well timed and adequately implemented.

What the administration executed between May and July 2023 was a simultaneous shock-on-shock policy combination: subsidy removal, naira float, electricity tariff increases, and monetary tightening, all within a compressed timeframe, which stopped the economic bleeding, but without a pre-positioned and adequately funded social protection buffer. The result was a cascading pass-through of cost increases across the entire economy. Transport costs exploded because fuel prices jumped from approximately ₦195 per litre to above ₦600. Because Nigeria’s informal logistics system is almost entirely fuel-cost sensitive, food prices followed within weeks. SMEs, already operating on thin margins in an import-dependent economy, found their input costs unrecognisable.

The naira has since settled in the ₦1,370–₦1,390 per USD range on the official window (February 2026 data). This represents a permanent structural repricing of the entire import-dependent Nigerian economy, and Nigeria imports almost everything that cannot be grown in a field or extracted from the ground.

Comparative development experience is instructive here. Indonesia’s post-Asian Financial Crisis adjustment under President Habibie and later Megawati, which included subsidy rationalisation, was accompanied by a deliberately structured social safety net (the Jaring Pengaman Sosial – Social Safety Net) that covered tens of millions of vulnerable households. South Korea’s response to the same crisis in 1997–1999, widely regarded as the most successful stabilisation-and-recovery sequence of that period, combined fiscal adjustment with targeted employment programmes, active industrial policy, and systematic workforce support. Ghana’s 2022–2024 IMF programme, even with its acute fiscal constraints, deployed the Livelihood Empowerment Against Poverty (LEAP) programme as a buffer for the poorest quartile.

Nigeria’s social protection architecture during the reform shock of 2023–2024 was, by contrast, fragmented, under-funded, and poorly targeted. The palliative distributions announced, both cash transfers and food items, were administratively overwhelmed, politically distorted, and grossly insufficient relative to the scale of household exposure. This is not a partisan verdict; it is the assessment of the World Bank in its April 2026 Nigeria Development Update, which observed that ‘household incomes have not grown fast enough to offset still-elevated inflation, and poverty has yet to begin declining.’

III. THE POVERTY PARADOX: MACRO RECOVERY AMID HOUSEHOLD DETERIORATION

Perhaps the most damaging empirical challenge to the administration’s recovery narrative comes from the World Bank’s Nigeria Development Update, released in April 2026. The report documents with clinical precision what policy analysts have long observed on Nigerian streets: that macroeconomic stabilisation and household welfare recovery are not the same thing, and that the former does not automatically or rapidly produce the latter.

The data is unambiguous. Nigeria’s poverty rate rose from 56% in 2023 to 61% in 2024, and further to 63% in 2025, the equivalent of approximately 140 million people living below the national poverty line (World Bank, April 2026). This trajectory occurred even as headline inflation was declining from its 34.80% peak in December 2024. The World Bank’s explanation captures the paradox precisely: ‘The persistence of poverty reflects the cumulative effects of earlier inflation spikes, which had already weakened real incomes before the recent easing in prices.’

In practical terms, what this means is that the sequence of shocks, subsidy removal, naira devaluation, tariff increases, compressed household real incomes so severely in 2023–2024 that even the subsequent moderation of inflation has not restored purchasing power. A bag of rice that cost ₦30,000 in early 2023 had risen to between ₦80,000 and ₦100,000 in many markets by 2025. Even if it has since retreated to ₦70,000–₦75,000, this is not experienced as relief by a household whose income has not risen proportionately.

Disinflation, a slower rate of price increase, is not the same as deflation. And disinflation without commensurate real wage growth does not restore living standards. This is the central empirical weakness in the administration’s claim that ‘food prices have largely come down.’

The NBS’s own data tells a nuanced story. Food inflation fell to 8.89% in January 2026, its lowest level in more than a decade, before rebounding to 14.31% in March and 16.06% in April 2026, the first time in eight months that food inflation had exceeded headline inflation (Nairametrics, May 2026). The World Bank notes that food inflation ‘disproportionately affects poor households who spend up to 70% of their income on food’ (World Bank, 2026). Nigeria’s national minimum wage of ₦70,000 per month, roughly USD 50 at current rates, means that the average formal sector worker is spending over ₦49,000 of their monthly income on food alone, before rent, transport, healthcare, or school fees are considered.

For the administration to claim, in a national address, that food prices have ‘largely come down,’ is to speak the language of year-on-year statistical comparison in a register that is simply unintelligible to the daily lived experience of Nigerian households. It is statistically defensible in a narrow technical sense. It is politically and morally disconnected from citizen reality.

IV. THE STOCK MARKET CELEBRATION: GROWTH FOR ENTREPRENEURSHIP & NOT THE MASSES

The President’s address makes much of the Nigerian Exchange Group’s All Share Index rising from 53,000 to 250,000, a near-fivefold increase, and market capitalisation expanding from ₦30 trillion to ₦160 trillion. These figures are factually correct. They also require substantial contextual disaggregation before they can be presented as evidence of broad-based economic recovery.

Capital market analysts and institutional economists have consistently noted that a significant proportion of Nigeria’s stock market expansion since 2023 reflects a well-documented phenomenon in high-inflation, currency-depreciating economies: hyper-inflationary asset repricing. When a currency loses more than 50% of its external value over twelve months, the naira-denominated valuations of assets, equities, real estate, and corporate balance sheets rise mechanically, even if the underlying productive assets have not grown in real terms. This is not wealth creation. It is a currency-denominated repricing of existing assets.

More fundamentally, the beneficiaries of Nigerian capital market growth are a sharply delineated segment of the population. The Nigerian capital market participation rate remains below 5% of the adult population. The growth in market capitalisation has primarily accrued to commercial banks reporting record nominal profits, energy sector companies, and large telecoms operators, entities that have been able to pass currency depreciation through to consumers via higher prices and tariffs. The Channels TV analysis of the anniversary address made this observation clearly: paper growth driven by currency devaluation benefits major corporations, not ordinary citizens.

To invoke stock market growth as evidence of recovery in a context where 140 million people are living below the poverty line is to confuse the health of financial markets with the welfare of citizens, a confusion that development economists have identified as one of the most persistent cognitive errors in emerging-market policy communication.

The speech would have been more credibly calibrated had it distinguished between what the capital markets data reflects, a stabilisation of the investor environment and a restoration of market confidence, and what remains deeply incomplete: the transmission of that macro-financial stability into household income, employment, and purchasing power.

V. THE POWER SECTOR: TWENTY COLLAPSES AND COUNTING

There is no single domain that more graphically illustrates the chasm between policy aspiration and citizen reality than Nigeria’s electricity sector. The President’s address acknowledges inherited failures and describes active reforms: clearing legacy obligations, expanding transmission infrastructure, attracting private investment, and decentralising the regulatory architecture through the Electricity Act 2023.

The data tells a grimmer story. Since President Tinubu took office in May 2023, Nigeria’s national grid has recorded no fewer than 20 collapses as of early 2026, according to industry data (Premium Times, May 2026). In 2024 alone, the grid failed approximately twelve times. Between 29 December 2025 and 27 January 2026, the grid collapsed three times in less than a month (Energy in Africa, March 2026). During the January 2026 collapse, power generation fell from 3,825MW to a catastrophic 39MW within minutes, a systemwide disturbance that plunged most of the country into darkness.

The structural dimensions of this crisis are not mysterious. Nigeria’s installed generation capacity stands at approximately 13,000MW, yet peak delivery to the grid in 2025 rarely exceeded 5,500MW and averaged closer to 4,000MW daily, roughly the consumption of a single mid-sized global city, serving a nation of over 200 million people and an estimated requirement of 30,000MW (BusinessDay, 2026). The gap between capacity and delivery reflects chronic gas supply failures, inadequate transmission infrastructure, the absence of a functioning SCADA (Supervisory Control and Data Acquisition) system for real-time grid management, and the financial distress of distribution companies that collected approximately ₦570 billion in Q3 2025 through tariff increases but could not fund adequate maintenance (ThisDay, 2026).

The Electricity Act 2023, passed in the administration’s first month, was a genuine structural milestone, replacing the 2005 Electric Power Sector Reform Act and enabling state governments and private investors to develop sub-national electricity markets. The National Integrated Electricity Policy, approved in 2025, provides a more comprehensive framework. But as Energy in Africa observed as recently as March 2026, ‘three years on, the reality on the ground raises a difficult question: if the law was designed to transform the market, then why are blackouts still dominating daily life?’

Nigeria has spent an estimated $33 billion on its power sector since the 2005 Electricity Power Sector Reform Act. By 2025, Egypt, with comparable population challenges, had achieved near-universal electricity access, after deliberate, sustained investment that more than doubled annual electricity sector spending between 2023 and 2026 (World Bank; Egypt MOEE, 2025). The contrast is instructive. Reform legislation, without funded delivery architecture and enforced regulatory accountability, remains an aspirational paper.

VI. AGRICULTURE AND FOOD SECURITY: THE SECURITY-FOOD NEXUS IGNORED

The administration’s agricultural interventions, input distribution, the National Agricultural Growth Scheme (NAGS-AP), and equipment deployment are presented in the third anniversary speech as meaningful progress toward food self-sufficiency and price reduction. The structural reality is more alarming.

The Food and Agriculture Organization of the United Nations (FAO) has warned that approximately 34.7 million Nigerians face acute food insecurity (IPC Phase 3 or worse) during the June–August 2026 lean season, projections contained in the Cadre Harmonisé analysis and confirmed by ACAPS’s April 2026 Nigeria situation report. FEWS NET’s April 2026 Food Security Outlook Update documents ongoing IED attacks on bridges and transport corridors in Kwara and Niger States, which are disrupting market access and preventing land preparation for the 2026 main agricultural season.

The Nigerian Security Tracker recorded over 1,200 people killed in violent incidents in the first quarter of 2025 alone, many in farming communities across Benue, Kaduna, Zamfara, Niger, and Plateau States. Banditry, kidnapping, and herder-farmer conflict have forced farmers across the North-West, North-Central, and Middle Belt to abandon their fields or pay extortionate sums for private security. ACAPS (2026) documents that security incidents in Nigeria’s BAY states (Borno, Adamawa, and Yobe) increased by 27% in the first quarter of 2026 compared to the same period in 2025.

You cannot achieve food self-sufficiency through agricultural input programmes in fields that farmers are too afraid to cultivate. The security-food nexus is the administration’s most critical governance failure, and its deepest omission from the anniversary address.

Agricultural transformation in contexts of conflict displacement requires, first and foremost, the restoration of security in farming communities. The developmental states of East Asia, South Korea, Taiwan, and later Vietnam, understood this sequencing instinctively: rural security and tenure stability came before the agricultural productivity revolution. Nigeria’s agricultural policy is attempting to run the productivity programme without first securing the field.

The administration’s CNG conversion programme for transportation, structurally sound in principle, remains ‘largely urban-locked.’ For the millions of rural transporters moving food from farms to markets across the North-West and North-Central corridors, CNG infrastructure is practically non-existent. This directly sustains food price inflation in urban markets even when farm-gate prices show some moderation.

VII. THE YOUTH AND BRAIN DRAIN CRISIS: NIGERIA’S LONG-TERM DEMOGRAPHIC EMERGENCY

President Tinubu’s address adopts the conciliatory and rhetorically sensitive posture toward youth, ‘You are not a problem to be managed’, that a government acutely aware of its approval ratings among younger demographics would predictably deploy. The sentiment is appropriate. The policy substance to match it remains inadequate.

Afrobarometer’s June 2025 dispatch on Nigerian youth, drawing on nationally representative survey data, documents that 23% of youth aged 18–35 report being unemployed and actively seeking work, though experts note that the official NBS unemployment methodology revision (from 53.4% to 6.5% for 15–24 year olds) has generated sustained academic controversy about whether official figures capture underemployment, informality, and desperate self-employment (Mbachu, African Business, 2025; NBS Labour Force Survey, 2024). The more structurally troubling finding is that six in ten Nigerian youth have considered emigrating, most to find jobs or escape economic hardship.

The ‘Japa’ phenomenon has evolved from a middle-class aspiration narrative into what clinicians and labour economists now increasingly describe as a survival strategy. A 2026 cross-sectional study published in the Nigerian Journal of Medicine, drawing on 1,200 clinical trainees across four training institutions, found that 60.8% of respondents intended to relocate abroad immediately after completing their training. Nigeria already has over 17,600 Nigerian-trained doctors practising in the United Kingdom alone, and approximately 5,400 in the United States (smartpreneur.ng, 2025). Nigeria’s doctor-to-patient ratio stands at 1:5,000, against the WHO standard of 1:600.

The issue of brain drain is not merely a healthcare statistic. It is a comprehensive signal of institutional failure, of a society that has ceased to be able to offer its most capable citizens a viable future within its borders. The ScienceDirect Japa-Japada framework (2025) identifies social, political, economic, and existential dimensions as the primary drivers of the phenomenon. Every professional who departs represents not only lost human capital but the accumulated public investment in their training, education subsidies, faculty salaries, clinical infrastructure, and redirected to the healthcare systems of the United Kingdom, Canada, and the Gulf States.

Nigeria’s median age is 18.1 years. Fifty-eight percent of the population is under 30 (World Bank, 2023; Worldometer, 2025). A nation this demographically young, with this degree of structural unemployment and talent exodus, is not experiencing a temporary adjustment cycle. It is experiencing the early stages of a human capital emergency that, if unaddressed within the next five to seven years, will permanently compromise its development trajectory.

The NELFUND student loan initiative presents President Tinubu with one of the clearest opportunities to reposition education as a central pillar of youth empowerment and national renewal. By expanding access to higher education through the disbursement of over ₦282 billion to more than 1.5 million students, the programme represents more than a welfare intervention; it is a strategic investment in Nigeria’s human capital. If sustained, strengthened and transparently managed, NELFUND can become a powerful bridge between economic reform and youth opportunity, especially for students from low-income families who might otherwise be excluded from tertiary education. While operational bottlenecks must be addressed, the initiative offers the administration a credible platform to demonstrate that reform is not only about fiscal stabilisation, but also about opening doors for the next generation of Nigerians.

VIII. INFRASTRUCTURE: THE ADMINISTRATION’S STRONGEST DOMAIN, WITH CAVEATS

If there is one domain where the administration’s narrative approaches credible alignment with observable reality, it is physical infrastructure. The Lagos-Calabar Coastal Highway, the Abuja-Kaduna-Zaria-Kano road rehabilitation, the East-West Road, and the Sokoto-Badagry Super Highway are real projects, with visible physical activity, and the infrastructure multiplier effect on logistics, trade corridor efficiency, and eventual employment is analytically sound.

The forensic caveats, however, are not minor. First, on sequencing: critics across the political spectrum have questioned the logic of committing trillions of naira to coastal mega-projects during a period of acute household food insecurity, collapsed real incomes, and deteriorating public health and education services. International development experience consistently cautions against prestige infrastructure prioritisation in contexts of acute social distress, a lesson that Myanmar, Venezuela, and several West African states have learned at severe cost.

Second, on transparency: the procurement structures, contractor accountability mechanisms, debt financing terms, and independent cost verification frameworks for these projects have not been made sufficiently public. Nigeria’s infrastructure sector has a documented institutional history of inflated contracts, politically motivated project awards, and incomplete delivery, a history that citizens reasonably invoke when evaluating current announcements.

Third, on completion risk: as the third-party forensic analysis correctly observes, ‘under construction, reconstruction, or rehabilitation’ is not ‘completed.’ Nigerian citizens, who remember the East-West Road saga spanning multiple administrations, increasingly judge governments by delivery certificates, not groundbreaking ceremonies.

IX. THE COMPARATIVE MIRROR: WHAT SUCCESSFUL REFORM SEQUENCES LOOK LIKE

The administration’s defenders will, correctly, point to the analytical consensus that macro-stabilisation must precede sustainable growth. They will cite South Korea’s 1997–1999 recovery, Indonesia’s post-crisis adjustment, and Rwanda’s post-1994 reconstruction as evidence that short-term pain can produce long-term transformation. These are legitimate comparisons, but they must be made with precision.

South Korea’s recovery from the Asian Financial Crisis was characterised by: (a) rapid, transparent communication of the reform programme’s logic; (b) a social compact that distributed sacrifices broadly and visibly, including among the chaebols and political elite; (c) active labour market intervention, including targeted retraining and employment subsidies; and (d) an institutional accountability architecture that prevented reform benefits from being captured exclusively by financial elites. The sacrifice was genuinely shared, and the recovery, when it came, was genuinely inclusive.

Rwanda’s developmental state model, which reduced poverty from 77.8% of the population in 2001 to 38.2% by 2016 (NISR, Rwanda), rested on an explicit, consistently executed social contract between government and citizens, transparent institutional accountability, measurable service delivery targets, and the systematic subordination of elite privileges to citizen outcomes.

Indonesia’s post-crisis stabilisation under the IMF programme was, in many respects, the cautionary tale rather than the success story: social safety net under-delivery generated severe political instability, contributing to President Suharto’s fall and years of democratic turbulence. The lesson that Indonesia’s subsequent leadership internalised, that the pace of stabilisation must be calibrated to the absorptive capacity of social systems, is directly relevant to Nigeria’s current moment.

Ghana’s 2022–2024 experience is perhaps the most instructive African parallel. The Akufo-Addo government’s simultaneous fiscal and monetary shocks, driven by debt distress and currency depreciation, produced macroeconomic stabilisation but severe electoral punishment in the 2024 elections, as the Mahama NDC swept back to power on the explicit platform of household cost relief. The political economy lesson is clear: citizens will grant governments one electoral cycle of patience for stabilisation; they will not grant a second unless they can feel the recovery in their daily lives.

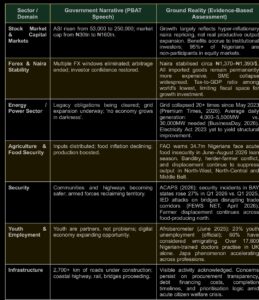

X. SCORECARD: SPEECH CLAIMS AGAINST EVIDENCE-BASED REALITY

The table below applies a systematic forensic lens to the major claims of the third anniversary address, drawing on data from NBS, World Bank, IMF, CBN, FAO, FEWS NET, ACAPS, and Afrobarometer

.

XI. THE DUAL NIGERIA PROBLEM: A CRISIS OF LEGITIMACY

The deepest analytical finding of this forensic review is not that the Tinubu administration’s reforms are wrong in direction. Most of the structural adjustments implemented since May 2023 were, as this paper acknowledges, economically necessary. The fiscal haemorrhage of the subsidy regime could not have been sustained. The multiple exchange rate windows were institutionally corrupt and economically destructive. The direction of travel is, in aggregate, defensible.

The crisis is one of distribution, sequencing, social protection adequacy, and institutional delivery. And it is producing what might be called the Dual Nigeria problem, a country that simultaneously hosts world-class macro-stabilisation metrics and world-class poverty indicators. A Nigeria where the Nigerian Exchange Group’s market capitalisation has grown to ₦160 trillion, and the World Bank simultaneously documents 140 million people below the poverty line. A Nigeria where GDP is growing at 3.89% (2025 estimate; CBN, 2025) while the IMF projects 2026 consumer price inflation at 16%, and the FAO projects 34.7 million people facing acute food insecurity in the June–August lean season.

These are not contradictory data points. They are the precise signature of what development economists call a ‘growth without inclusion’ trajectory, the classic failure mode of reform programmes that stabilise financial aggregates without simultaneously investing in the human and social infrastructure that translates macro gains into citizen welfare.

The political economy risk is acute. History across emerging markets is unambiguous: populations will tolerate macroeconomic restructuring if they believe its benefits will reach them within a perceptible timeframe. Nigeria is now in its third year of stabilisation. The fourth year will be an election year. The administration’s political survival depends not on what the economists say about Nigeria, but on what the trader in Onitsha, the teacher in Zaria, and the graduate in Port Harcourt feel about their own lives.

CONCLUSION: STABILISATION IS NOT RECOVERY — AND THE CLOCK IS TICKING

President Tinubu’s third anniversary address is, on its own terms, a politically disciplined document. It demonstrates macroeconomic coherence, rhetorical sophistication, and a selective but technically accurate command of stabilisation data. It will resonate in investor boardrooms, multilateral briefing rooms, and among the diaspora elites who follow Nigeria’s macro story from a distance.

But a forensic analysis must conclude that the speech suffers from three fundamental inadequacies. First, it conflates macro-stabilisation with recovery, when the World Bank, IMF, and NBS data collectively demonstrate that 140 million Nigerians are living in deepening poverty even as top-line economic indicators improve. Second, it systematically under-addresses the structural drivers of household distress, insecurity, power sector collapse, youth unemployment, and the brain drain crisis, which are not amenable to macroeconomic medicine alone. Third, it makes the fundamental communications error of speaking to aggregate statistics in a register that is unintelligible to citizens whose primary economic experience is the cost of a bag of rice or pepper.

The administration has demonstrated that it can stabilise an economy in distress. That is a genuine, difficult achievement. The question that will determine its historical judgment, and its political survival, is whether it can now build the bridge from stabilisation to inclusion. From reform metrics to citizen reality. From the recovery that economists see, to the recovery that a mother in Kano, a farmer in Benue, or a newly graduated engineer in Lagos can actually feel.

That is the challenge we address in Part II of this series: the architecture of inclusive recovery, moving from macro-stabilisation to grassroots development through targeted social investment, security-first agricultural policy, power sector delivery reform, and a youth retention compact. The roadmap exists. The question is whether the political will to execute it, at the pace that citizen welfare demands, is equally present.

Nigeria’s reform story is not yet written. But the next chapter belongs not to the stabilisation economists, it belongs to the social architects. And the clock is ticking.

REFERENCES AND DATA SOURCES

A. Institutional and Policy Documents

African Development Bank (AfDB). (2025/2026). African Economic Outlook 2025/2026. Abidjan: AfDB Group.

ACAPS. (2026). Nigeria Situation Report, April 2026. Geneva: Assessment Capacities Project.

Central Bank of Nigeria (CBN). (2025, December). Macroeconomic Outlook for Nigeria, 2026. Abuja: CBN.

Famine Early Warning Systems Network (FEWS NET). (2026, April). Nigeria Food Security Outlook Update: April–September 2026. Washington, D.C.: USAID.

Food and Agriculture Organization (FAO). (2025, October). Cadre Harmonisé: Nigeria Acute Food and Nutrition Insecurity Analysis. Rome: FAO/CILSS.

Food and Agriculture Organization (FAO). (2025, March). Projected Acute Food and Nutrition Insecurity 2025 Lean Season. Rome: FAO.

International Monetary Fund (IMF). (2025, July). Article IV Consultation — Nigeria. Washington, D.C.: IMF. [IMF projects 2026 real GDP growth at 4.1%; consumer prices at 16.0%]

IMF. (2023). Nigeria: Staff Statement on Exchange Rate Policy. Washington, D.C.: IMF.

National Bureau of Statistics (NBS). (2026, April). Consumer Price Index Report — March 2026. Abuja: NBS.

National Bureau of Statistics (NBS). (2026, May). Consumer Price Index Report — April 2026. Abuja: NBS.

National Bureau of Statistics (NBS). (2024). Nigeria Labour Force Survey: Q2 2024. Abuja: NBS.

National Institut of Statistics of Rwanda (NISR). (2016). Rwanda Integrated Household Living Conditions Survey. Kigali: NISR.

World Bank. (2026, April). Nigeria Development Update: Nigeria’s Tomorrow Must Start Today — The Case for Early Childhood Development. Washington, D.C.: World Bank. [Documents poverty rate rise to 63% / ~140m people in 2025]

World Bank. (2025, October). Nigeria Development Update: Building Momentum for Inclusive Growth. Washington, D.C.: World Bank.

World Bank. (2026). Nigeria Country Overview and CPF FY2021–2025. Washington, D.C.: World Bank. [Notes 60%+ poverty; food-poor households spend up to 70% of income on food]

. Academic and Research Publications

Akinwale, A. A., & George, T. O. (2023). Medical brain drain from Nigeria: A systematic review. African Journal of Health Sciences, 36(2), 114–129.

Mbachu, D. (2025). Nigeria’s revamp of economic indicators sparks debate. African Business. March.

Nigerian Journal of Medicine. (2026, April). Perception of clinical medical trainees on international relocation from Nigeria (‘Japa’ syndrome) after graduation. Vol. 35(1). [60.8% of clinical trainees intend to relocate abroad immediately]

Obi-Ani, N. A., Isiani, M. C., & Obi-Ani, P. (2022). Social media and the ‘Japa’ syndrome among Nigerian youth. Cogent Social Sciences, 8(1).

ScienceDirect. (2025, May). The ‘Japa-Japada’ construct: A theoretical framework for exploring the recent medical brain drain scourge in Sub-Saharan Africa. [Social, political, economic, existential dimensions ranked as primary drivers] DOI: 10.1016/j.healthpol.2025.00641.

United Nations Development Programme (UNDP). (2024). Human Development Report 2023/2024: Breaking the Deadlock. New York: UNDP.

C. Survey and Barometer Data

Afrobarometer. (2025, June 16). Dispatch No. 998: Facing lack of economic opportunity, Nigerian youth want government action on jobs and cost of living. Accra: Afrobarometer. [23% youth unemployment; 60% considered emigrating; median age 18.1 years]

NOIPolls. (2024). Nigeria Economic Perception Survey, Q3 2024. Lagos: NOIPolls.

D. Media and Data Platforms Cited

BusinessDay NG. (2026, January 23). Nigeria’s power grid collapses for first time in 2026. BusinessDay.

Energy in Africa. (2026, March 23). Nearly three years after overhauling electricity law, Nigeria’s power crisis worsens.

FEWS NET. (2026, April). Conflict and rising input costs driving Crisis (IPC Phase 3) in northern Nigeria.

Nairametrics. (2026, May 18). Nigeria’s food inflation surpasses headline rate for first time in eight months.

Premium Times. (2026, May). Nigeria’s new power minister pledges to fix grid collapse. [Grid recorded 20+ collapses since May 2023]

Punch Nigeria. (2026, April 15). Inflation rises to 15.38% as food, transport costs bite.

The Guardian Nigeria. (2026, April). Nigeria’s inflation rises to 15.38% in March 2026 as CPI hits 135.4.

ThisDay Live. (2026, January 18). Nigeria’s electricity paradox and the unanswered question of 2026.

Vanguard Nigeria. (2026, February 9). Frequent national grid collapses and the shame of a nation.

E. Comparative Country References

Bank of Korea. (1999). Annual Report: Economic Stabilisation and Recovery. Seoul: Bank of Korea.

Ghana Ministry of Finance. (2023). IMF-Supported Programme: Domestic Debt Exchange Programme. Accra: MoF Ghana.

Indonesia National Planning Agency (BAPPENAS). (1999). Recovery Programme Documentation: Jaring Pengaman Sosial (JPS). Jakarta: BAPPENAS.

World Bank. (2025). Egypt Electricity Sector Overview and Investment Data, 2025–2026. Washington, D.C.: World Bank.

About the Authors

Prof. Sarumi, a digital transformation architect and leadership strategist with over 40 years of cross-sector experience across Nigeria and the African continent.

Prof. Olusola O. Aliu is a researcher, Entrepreneurship and policy analyst, with over 50 years multidisciplinary sectors specialising in Nigerian political economy and institutional reform across Europe and the African continent,

© 2026 Oyewole O. Sarumi PhD & Olusola O. Aliu PhD. All rights reserved. Part II of this series will address the ar

chitecture of inclusive recovery

{kind=link}